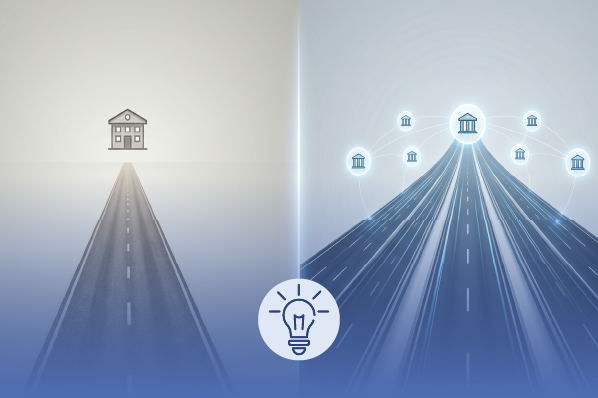

A multi-lender financing platform is software that sits between a merchant's point of sale and a network of many different lenders, then routes a single customer application across those lenders to maximize the odds of approval and the quality of the offer the customer receives. One application replaces a sales associate asking a customer to apply with one bank, then another, then another — each one chipping at the customer's credit score and at the patience that closes the sale.

The mechanic underneath is the financing waterfall: the application starts at the top tier (typically a prime lender), and if that lender declines or the customer doesn't accept the offer, the application falls through to the next tier, and the next, until someone approves. From the customer's perspective, it is one form, one decision, one payment plan. From the merchant's perspective, it is the difference between losing the sale on the first decline and capturing it on the fourth.

How a multi-lender platform actually works

A customer at the point of sale fills out a single application. The platform runs a soft credit pull at the top of the cascade so the customer's score isn't pulled multiple times. The application is then submitted to lenders in sequence, in parallel, or in a hybrid pattern — depending on how the platform is configured. Each lender returns an approval, a partial approval, or a decline. The platform presents the best offer the customer qualifies for. The merchant collects the sale.

The deeper the lender stack and the more sophisticated the routing logic, the higher the approval coverage. Merchants who switch from a single-lender setup to a real multi-lender waterfall commonly move from 40–60% approval rates to 70–90%+ overall approval coverage — depending on the lineup and the credit mix of their customer base.

What separates a real multi-lender platform from a lender that has a few partners

The category gets described loosely, so it's worth being precise. A real multi-lender platform has three things working together:

Lender breadth across the full credit spectrum — prime, near-prime, subprime, lease-to-own, and (in the best implementations) an in-house plan tier for customers who have the means but not the credit profile. A platform with only prime and near-prime is a single-tier shop with a fallback, not a waterfall.

Routing intelligence that goes beyond a static lender order — the order of lenders shifts based on cart size, vertical, customer signals, and historical approval data. Smart routing closes sales static routing leaves on the table.

Unified merchant economics and reporting — one set of fees, one dashboard, one place to see approval rates, financed revenue, and lender performance across every tier. A platform that hands you a different login per lender isn't a platform, it's an aggregator of friction.

Why the model exists

Any single lender only approves a slice of applicants. A prime lender approves strong-credit buyers and declines everyone else. A near-prime lender catches the middle band. A subprime or lease-to-own provider covers the rest. A merchant tied to one lender loses the sale every time that lender says no — even though another lender on the same application would have said yes. The waterfall exists to close that gap automatically.

The model emerged in retail because big-ticket purchases — furniture, jewelry, medical and dental procedures, home improvement, auto repair, pet and veterinary care, education — are where financing converts a browser into a buyer. Every incremental approval drops straight to the merchant's close rate and average ticket.

The category is consolidating around a single architecture

Versatile Credit (acquired by Synchrony), ChargeAfter, FinMkt, LendPro, and FormPiper are all instances of the multi-lender platform model. They diverge on lender depth, vertical specialization, in-house payment support, embed UX, and pricing model — but the underlying architecture is the same: one application, many lenders, dynamic routing, unified reporting.

The meaningful question for any operator evaluating the category isn't whether to adopt a multi-lender platform — the math has decided that. The meaningful question is whether the platform you choose stays an independent router across many lenders, or eventually gets absorbed into a single lender's balance sheet. That independence-vs-captive argument is the active competitive frontier in the space, and it is the question every retailer should ask their financing vendor before signing.

Frequently Asked Questions

Is a multi-lender platform the same as a financing waterfall?

Yes. "Waterfall lending," "cascading approvals," "multi-lender orchestration," and "multi-lender platform" all describe the same architecture: one application, many lenders, routed in sequence or parallel until someone approves.

How much approval lift can a merchant expect?

Merchants moving from a single-lender setup to a real multi-lender waterfall typically move from 40–60% approval rates to 70–90%+ overall coverage. The exact lift depends on the customer credit mix and the depth of the lender stack.

Does a multi-lender platform pull credit multiple times?

A well-implemented platform runs a soft pull at the top of the waterfall so the customer's credit isn't dinged on every attempt. Only when the customer accepts an offer does a hard pull happen — and only with the lender whose offer was accepted.

Which industries use multi-lender platforms most?

Furniture, jewelry, medical and dental, home improvement, auto repair, pet and veterinary, and education are the most common verticals — anywhere ticket sizes are large enough that financing decides whether the sale closes.

How does FormPiper's multi-lender platform compare?

FormPiper runs the waterfall, credit card processing, and an in-house payment tier through one platform — built for independent retailers who want every payment moment handled end-to-end. Six tiers (Prime, Near Prime, Sub Prime, Lease to Own, In-House, Credit Card), dynamic routing, flat enterprise pricing.

See FormPiper's multi-lender platform in action. Get Your Custom Demo

.png?width=1278&height=333&name=Logo%20FormPiper%20Horizontal%20Full%20Color%20(1).png "Logo FormPiper Horizontal Full Color (1)")